Why are we building Munch?

Why are we building Munch?

To solve for the anxiety associated with money.

In the summer of 2017, I found myself studying for the CFA exams at quiet coffee shops. Unfortunately for my bank balance, those were the only places I could focus at for long hours. Young and broke, I tried to keep a strict tab on the rest of my money. I didn't realize exactly how hard that would be.

Fast forward a few years and not much has changed. I started earning more money but I was still clueless about where it went. Frustrated, I resigned my Sunday mornings to sitting in front of a spreadsheet.

Despite coming from a background in finance, I faced this problem. Gathering the information to analyse what you spent on was too cumbersome. Nobody’s got the time for that. Even after trying most of the available solutions, nothing stuck. Friends from non-finance backgrounds also complained of the jargon required to understand and manage money. The system didn't make it any easier either.

This process pointed to a few fundamental problems in our financial system. The "undemocratic" nature of this industry was clear. Financial advisors target older individuals with greater wealth, a more lucrative market.

Younger individuals are not prioritized as a core target group due to lower disposable income. As a result, we lose out on the benefits of compounding 💰 by not starting early.

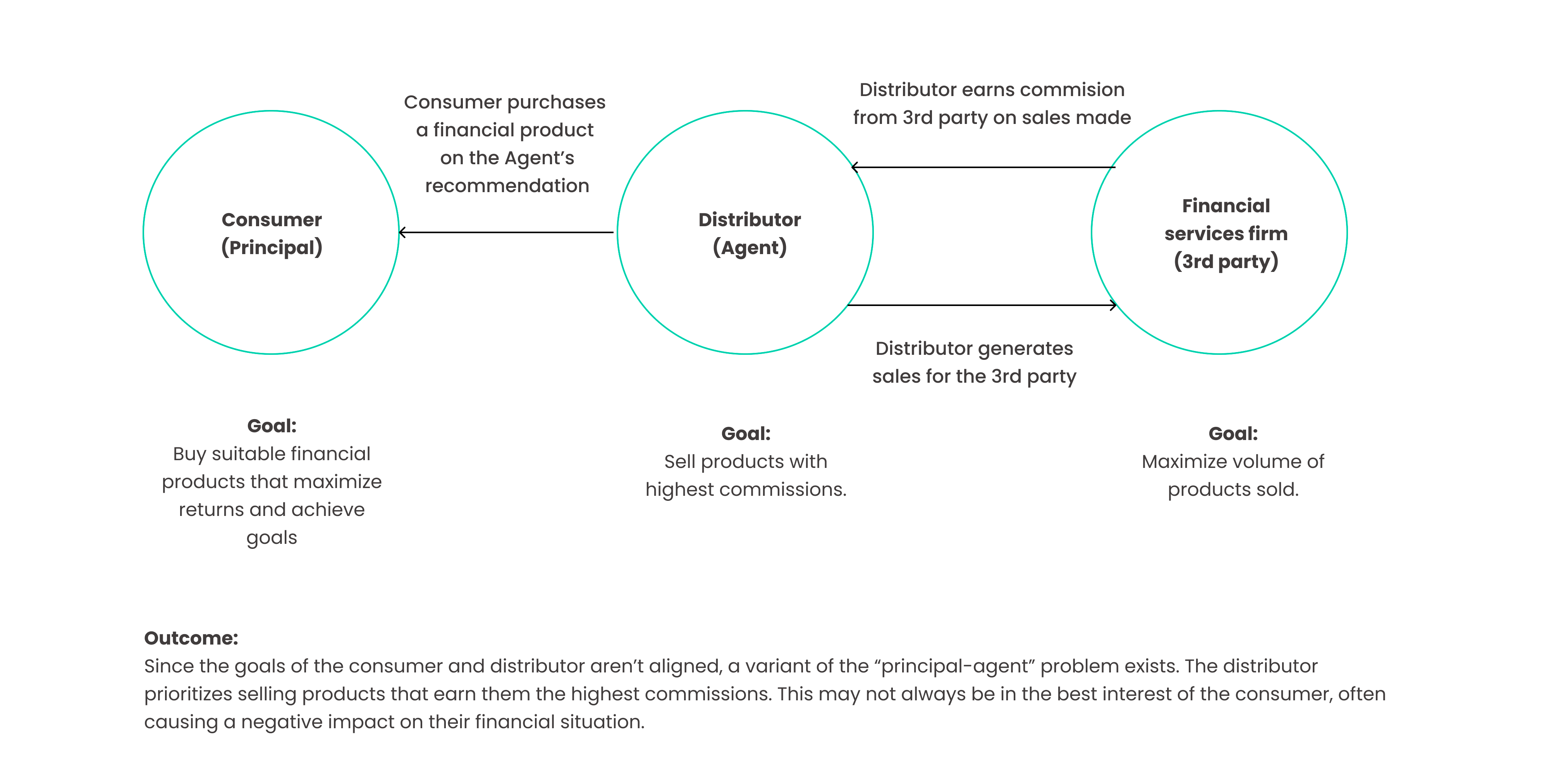

The average Indian hesitates to pay for financial planning and investment advice. Instead, they turn to the distributor selling financial products for recommendations. Incentivized to sell products that fetch the highest commissions, distributors have a conflict.

As a result, the average individual has ended up with products not always suitable for them. The classic Principal-Agent problem. In a welcome move, the SEBI recently decided to do something about it (read more about it here 👉 link).

All these put together forced us to pay closer attention.

Who are we? And… what are we doing? 🤷♀️

We're a group of young hackers and finance professionals. Frustrated by how difficult it is to successfully navigate the financial system today, we want to create a solution that addresses that.

Thinking deeper, we realised why we should do this 👇

Millennials and Gen Z form a majority of the working population in this country. This will be the case for the next few decades. Digital payments and e-commerce are a key feature of our lives. Fulfilling all needs and desires is easier than ever before. Unfortunately, so is falling into the trap of consumerism through credit card debt, among others.

Due to the jargony, time consuming, and boring nature of financial services, it's easier to not make any decisions at all. This applies especially to young adults. By not starting early, we likely give up a more favorable life trajectory.

The choices we make with our money have a “butterfly effect” on our economy, far more powerful than we can imagine. A country like India can’t afford any version of the 08-09 crisis (even the mildest).

All these nuances generated a sense of urgency in us to take a legitimate swing at this problem. We quit our jobs in the middle of the pandemic to dive into it.

Each one of us has unique lives, goals and aspirations. A manual, one-size fits all approach with basic heuristics is no longer the answer.

To start with, we’re attempting to make investing concepts fun on our 📲 Instagram & LinkedIn pages. We’re also starting a series that takes aim at the taboo associated with money.

Through the stories of urban, young Indians and their journey with money, we aim to destigmatize this topic. We believe that by encouraging healthy and open conversations, we all stand to learn from each other and improve our relationship with money.

✨✨If you relate to what we’re talking about and would like to know more, give us a holler on our social media handles. We love to make new friends, discuss these problems, and figure out ways to help. We'd love to duct-tape your money-related problems while we build a sustainable solution. ✨✨